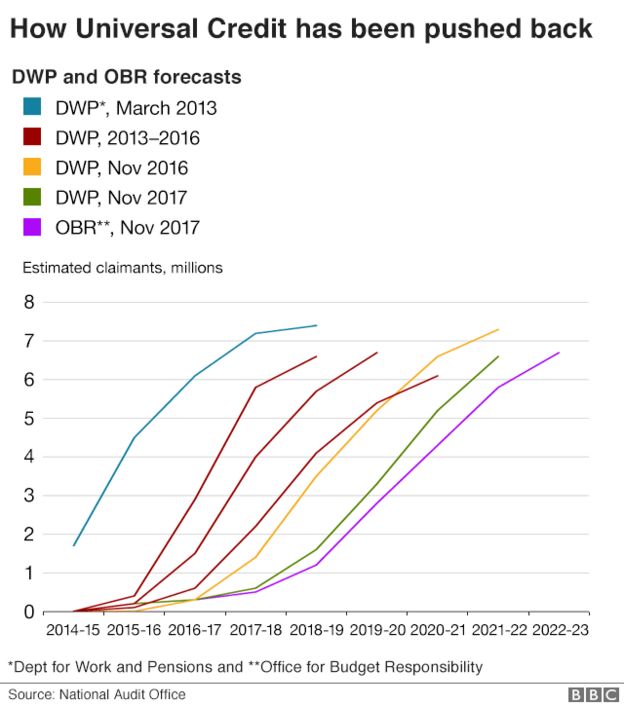

A major fraud has been reported affecting Universal Credit. Over the course of the last eight and a half years, I’ve frequently commented on the vulnerability of the UC system to fraud and error, despite repeated assertions from the government – and the falsification of the business case – to claim the opposite. This fraud is different from most, because it represents organised criminal activity that is neither attributable to claimants nor to DWP officials. The criminals pretend to be other people, both claimants and people who have not claimed, to register for short term loans before any checks might be made. (This is not, for the most part, ‘identity theft’; it is personation. A fraud of this sort is typically a fraud on the DWP, not on the claimaint.)

It should have been obvious from the outset that computer-based identification wouldn’t be sufficiently secure for the purposes of the DWP. There was something close to an admission of this more than three years ago, when Verify, the successor to the failed “Identity Assurance”, was cut adrift. But the problem is not only down to poor tech. The situation has been produced by a system that relied on online verification, rather than claims in person; that left claimants without resources for well over a month; and replaced a system capable of processing the vast majority of claims within 14 days with one that struggled to do it in six weeks, and sometimes could take as long as three months. Universal Credit is error-prone by design. Its vulnerability to deception is only a part of that.